Global Semiconductor Capacity Projected to Reach Record High 30 Million Wafers Per Month in 2024, SEMI Reports

Milpitas, Calif., (ANTARA/PRNewswire)- Global semiconductor capacity is expected to increase 6.4% in 2024 to top the 30 million *wafers per month (wpm) mark for the first time after rising 5.5% to 29.6 wpm in 2023, SEMI announced today in its latest quarterly World Fab Forecast report.

The 2024 growth will be driven by capacity increases in leading-edge logic and foundry, applications including generative AI and high-performance computing (HPC), and the recovery in end-demand for chips. The capacity expansion slowed in 2023 due to softening semiconductor market demand and the resulting inventory correction.

"Resurgent market demand and increased government incentives worldwide are powering an upsurge in fab investments in key chipmaking regions and the projected 6.4% rise in global capacity for 2024," said Ajit Manocha, SEMI President and CEO. "The heightened global attention on the strategic importance of semiconductor manufacturing to national and economic security is a key catalyst of these trends."

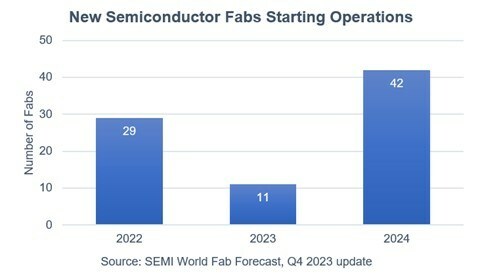

Covering 2022 to 2024, the World Fab Forecast report shows that the global semiconductor industry plans to begin operation of 82 new volume fabs, including 11 projects in 2023 and 42 projects in 2024 spanning wafer sizes ranging from 300mm to 100mm.

China Leads Semiconductor Industry Expansion

Boosted by government funding and other incentives, China is expected to increase its share of global semiconductor production. Chinese chip manufacturers are forecast to start operations of 18 projects in 2024, with 12% YoY capacity growth to 7.6 million wpm in 2023 and 13% YoY capacity growth to 8.6 million wpm in 2024.

Taiwan is projected to remain the second-largest region in semiconductor capacity, increasing capacity 5.6% to 5.4 million wpm in 2023 and posting 4.2% growth to 5.7 million wpm in 2024. The region is poised to begin operations of five fabs in 2024.

Korea ranks third in chip capacity at 4.9 million wpm in 2023 and 5.1 million wpm in 2024, a 5.4% increase as one fab comes online. Japan is expected to place fourth at 4.6 million wpm in 2023 and 4.7 million wpm in 2024, a capacity increase of 2% as it starts operations of four fabs in 2024.

The World Fab Forecast shows the Americas increasing chip capacity by 6% YoY to 3.1 million wpm with six new fabs in 2024. Europe & Mideast is projected to up capacity 3.6% to 2.7 million wpm in 2024 as it launches operations of four new fabs. Southeast Asia is poised to increase capacity 4% to 1.7 million wpm in 2024 with the start of four new fab projects.

Foundry Segment Continues Strong Capacity Growth

Foundry suppliers are forecast to rank as the top semiconductor equipment buyers, increasing capacity to 9.3 million wpm in 2023 and a record 10.2 million wpm in 2024.

The memory segment slowed expansion of capacity in 2023 due to weak demand in consumer electronics including PCs and smartphones. The DRAM segment is expected to increase capacity 2% to 3.8 million wpm in 2023 and 5% to 4 million wpm in 2024. Installed capacity for 3D NAND is projected to remain flat at 3.6 million in 2023 and rise 2% to 3.7 million wpm next year.

In the discrete and analog segments, vehicle electrification remains the key driver of capacity expansion. Discrete capacity is forecast to grow 10% to 4.1 million wpm in 2023 and 7% to 4.4 million wpm in 2024, while Analog capacity is projected to grow 11% to 2.1 million wpm in 2023 and 10% to 2.4 million wpm in 2024.

The latest update of the SEMI World Fab Forecast report, published in December, lists 1,500 facilities and lines globally, including 177 volume facilities and lines with various probabilities expected to start operation in 2023 or later.

Download a sample of the SEMI World Fab Forecast report.

For details about SEMI reports on other semiconductor sectors, visit SEMI Market Data or contact the SEMI Market Intelligence Team (MIT) at mktstats@semi.org.

*200mm equivalent

About SEMI

SEMI® connects 3,000 member companies and 1.3 million professionals worldwide to advance the technology and business of electronics design and manufacturing. SEMI members are responsible for the innovations in materials, design, equipment, software, devices, and services that enable smarter, faster, more powerful, and more affordable electronic products. Electronic System Design Alliance (ESD Alliance), FlexTech, the Fab Owners Alliance (FOA), the MEMS & Sensors Industry Group (MSIG), Nano-Bio Materials Consortium (NBMC), and SOI Consortium are SEMI Strategic Technology Communities. Visit www.semi.org, contact one of our worldwide offices, and connect with SEMI on LinkedIn and X (formerly Twitter) to learn more.

Association Contacts

Michael Hall/SEMI US

Phone: 1.408.943.7988

Email: mhall@semi.org

Christian G. Dieseldorff/SEMI US

Phone: 1.408.943.7940

Email: cdieseldorff@semi.org

Chih-Wen Liu/SEMI Taiwan

Phone: 886.3.560.1777

Email: cwliu@semi.org

Source: SEMI